Case

How Swatch Saved the Swiss Watch Industry, But Not From Quartz

Swiss watches accounted for over 80% of the global watch market in 1945. Yet, by the time the 1970s wrapped up, the industry was dying.

National production declined from 96 million units in 1974 to 45 million in 1983. Employment plummeted from 89,000 workers in 1970 to 33,000 in 1985. And the flagship watchmaking group, SSIH (Société Suisse pour l’Industrie Horlogère), saw its sales volume fall from 12.4 million watches in 1974 to a measly 1.9 million in 1982.

Accounting for more than half of the Swiss watchmaking workforce, SSIH and its counterpart ASUAG (Allgemeine Schweizerische Uhrenindustrie AG) were insolvent by the start of the 80s. Top brands like Omega, Tissot, and Longines, having subsisted on emergency credit lines for years, were now verging on liquidation.

This was a shock. After centuries of success, the nation of proud watchmakers had been overtaken by innovative Japanese manufacturers. This threat started out slow. Japanese watchmakers developed a price and quality advantage during the early 70s. They eventually turned to quartz, a revolutionary — and disruptive — timekeeping technology they had perfected, to deliver a far better product at a much lower price. Years later, this entire period would be called the ‘Quartz crisis’, although quartz wasn’t exactly what caused the Swiss watch industry to decline so severely.

In 1982, Swiss creditor banks decided enough was enough. It was time for an exit strategy. So, they brought in Nicolas Hayek, a Lebanese-born businessman who, in 1963, pawned his household furniture to fund his fledgling consultancy business. By the late 1970s, that consultancy business was thriving, advising over 300 corporate clients, including Siemens and Nestle.

What did the bankers want?

According to Hayek’s obituary: “To plan the ordered bankruptcy of the remaining national watch industry.” However, Hayek had other ideas. What happened next was one of the most unlikely industrial comebacks in modern history. In so doing, the Swiss watch industry pulled off something highly unusual. The academics Hugues Jeannerat and Olivier Crevoisier argue that the Swiss — led by Hayek and a handful of other insiders — engaged in a form of ‘non-technological innovation’ that allowed them to compete with the continuous technical innovation coming out of Japan. This approach put them in good stead even in the decades after the crisis.

This is the story of what they did, and how they did it.

Swiss Dominance

The art of Swiss timepiece production dates back to the 16th century. At that time, Geneva was awash with skilled artisans, goldsmiths, and jewelry makers who crafted elaborate ornaments and personal adornments for the city’s wealthy patrons.

But, as the theologian John Calvin rose to political prominence in the 1540s, that market evaporated. A pious reformer, Calvin believed in an outright rejection of vanity. He imposed a jewelry ban, with one exception: personal timepieces — such as pocket watches — were permitted, as they weren’t simply “vain” decorations but rather valuable tools.

Experienced craftspeople saw the writing on the wall. They already possessed the skills — precision metalwork, decorative engraving, stone setting, miniaturisation — that could be transferred to timepiece making. And so they switched. Booming markets for timepieces in London, Paris, and Amsterdam drove rapid expansion. By 1760, Geneva had 800 master watchmakers, employing 4,000 workers, churning out 85,000 timepieces annually.

In the nearby Franche-Comté region of France, horologist Frédéric Japy was working throughout the 1770s to mechanize the production of watch components, developing a standardized system he called ébauche. Japy’s innovation was to provide prefabricated movement blanks, the skeleton parts of a watch, which artisans could use to assemble a watch in a fraction of the time they had previously.

Japy’s innovation didn’t take immediately, however. The uptake of ébauche in Swiss watchmaking emerged in response to an early threat. In the late 1870s, American watchmakers were the first to mass produce mechanical watches. Jacques David, an engineer from Longines, returned from a visit to America in 1876 and published a report, urging his fellow watchmakers to ‘wake up’ to the threat of American watch manufacturing. He explained that the Americans had standardised watch parts, had organised as vertically integrated houses, were machining components, and were therefore able to produce large volumes of inexpensive mechanical watches. His fellow watchmakers took heed; widespread adoption of the ébauche method of production occurred shortly after. Indeed, in 1870, Swiss watchmakers produced 1.6 million units whilst their closest competitor, France, produced 300,000. But by 1890, the Americans had dethroned France as the second-largest watchmaking nation, and was quickly seen as the Swiss’s largest competitor. Before Swiss watchmakers reacted — thanks in part to David’s report — the average American worker produced 150 watches per year, compared to a mere 40 for his Swiss counterpart.

Between 1885 and 1913, annual Swiss watch exports climbed steadily from three million to 10 million. Swiss watches dominated the market, gained a reputation for quality and craftsmanship, and this climb continued unabated … until the First World War.

A new threat emerged in the wake of WWI. This was known as chablonnage — the practice of exporting disassembled watches (such as movements or movement parts) and then assembling them in the countries in which they are sold. The main goal of this practice was to avoid high customs duties on completed watches. Chablonnage contributed to the expansion of the Bulova watch company in the US, and Citizen Watch in Japan. It wasn’t long before Swiss watchmakers noticed.

The Swiss watch industry had switched to armament production during the Great War, which ended in 1918. In the post-war period, the industry was saddled with an oversized industrial base and suffered from continually dropping prices thanks to an uneven post-war economic recovery. This presaged two crises: one during 1920 to 1922, and another from 1930 to 1936 (this second crisis was triggered by the Great Depression). In both cases, multiple firms went bankrupt and unemployment spiked. In both cases, Swiss watchmakers saw chablonnage as the major problem. Their great fear was tech transfer — emerging competitors in other countries could study the movements they imported, and then grow to challenge Swiss dominance.

And so it was during this period that the Swiss changed the structure of their entire industry. In 1934, the state passed the Statut horloger (the ‘Watchmaking Statute’), which formalised a watch cartel. By this time, Swiss manufacturers had already attempted to organise into cartels in response to chablonnage. For instance, many of the movement makers were consolidated into Ébauche SA, which made it easier to set industry-wide production, pricing, and export policies for Swiss-made movements. (The holding companies could then bully the holdout firms … though this didn’t always work). But then the Statut made such practices law. When the Great Depression hit in 1929 and Swiss watchmakers suffered, the industry created Allgemeine Schweizerische Uhrenindustrie AG (ASUAG) in 1931, to further concentrate parts manufacturing. Ébauche SA was parked under ASUAG, along with other parts manufacturers. As a result, all Swiss movements, movement blanks, and mainsprings outside of the ‘manufactures’ were concentrated within ASUAG — a single super holding company.

The other major consequence of the Statut was that 36 high end watch manufactures — that is, houses that included Rolex, Longines, Patek Phillippe, Tissot, Omega, Vacheron Constantin, and others — were now legally required to produce their own calibres. (Calibres were the watch movements that power a mechanical watch.) In other words, the Statut consolidated most firms, but forced independence for the highest end watchmakers.

Nearly all of these high-end manufactures chose not to adopt mass production techniques for their high-quality watches. The one exception to this was Rolex, who for idiosyncratic reasons did invest in modern production techniques for their top-end watches. Many of the manufactures then decided to pursue the low-end of the market, where they applied mass production techniques to shitty mechanical watches.

This industry structure would come to haunt them in the 1970s.

A Disruption — But Not of Quartz

The typical narrative of the Quartz Crisis goes something like this: in the early 70s, the Japanese watch company Seiko took quartz, then a nascent watch movement technology — and perfected it. By the end of the 90s quartz watches were both significantly cheaper and more accurate than mechanical watches. Seiko then licensed it to many other Japanese manufacturers. Cheap, accurate quartz watches flooded international markets, eating away at Swiss market share, triggering a crisis. This is therefore a tale of straightforward technological disruption. But for the genius of Nicolas Hayek, who came in and created the Swatch group, it is a wonder that the Swiss even survived.

This narrative, whilst popular, is wrong.

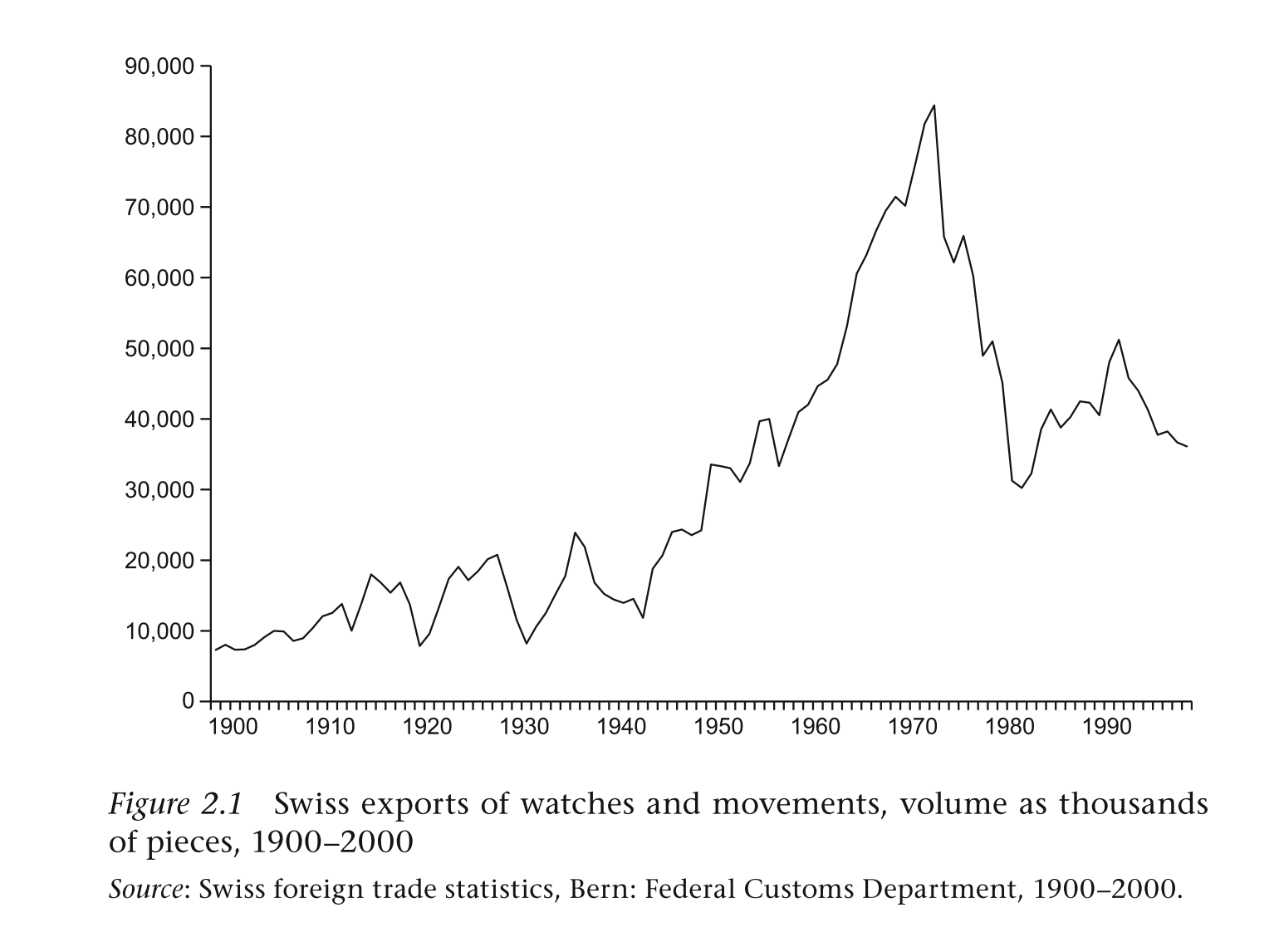

Pierre-Yves Donzé, the greatest living historian of the watch industry, uses two simple graphs to debunk this story.

The first graph shows Swiss national exports of watches and movements from 1900 to 2000. The graph spikes upwards from the mid 1940s through to the early 1970s, where it peaks at 84.4 million in 1974. The number of exports then looks like it falls off a cliff. It plunges at an alarmingly steep rate from 1975 to 1984.

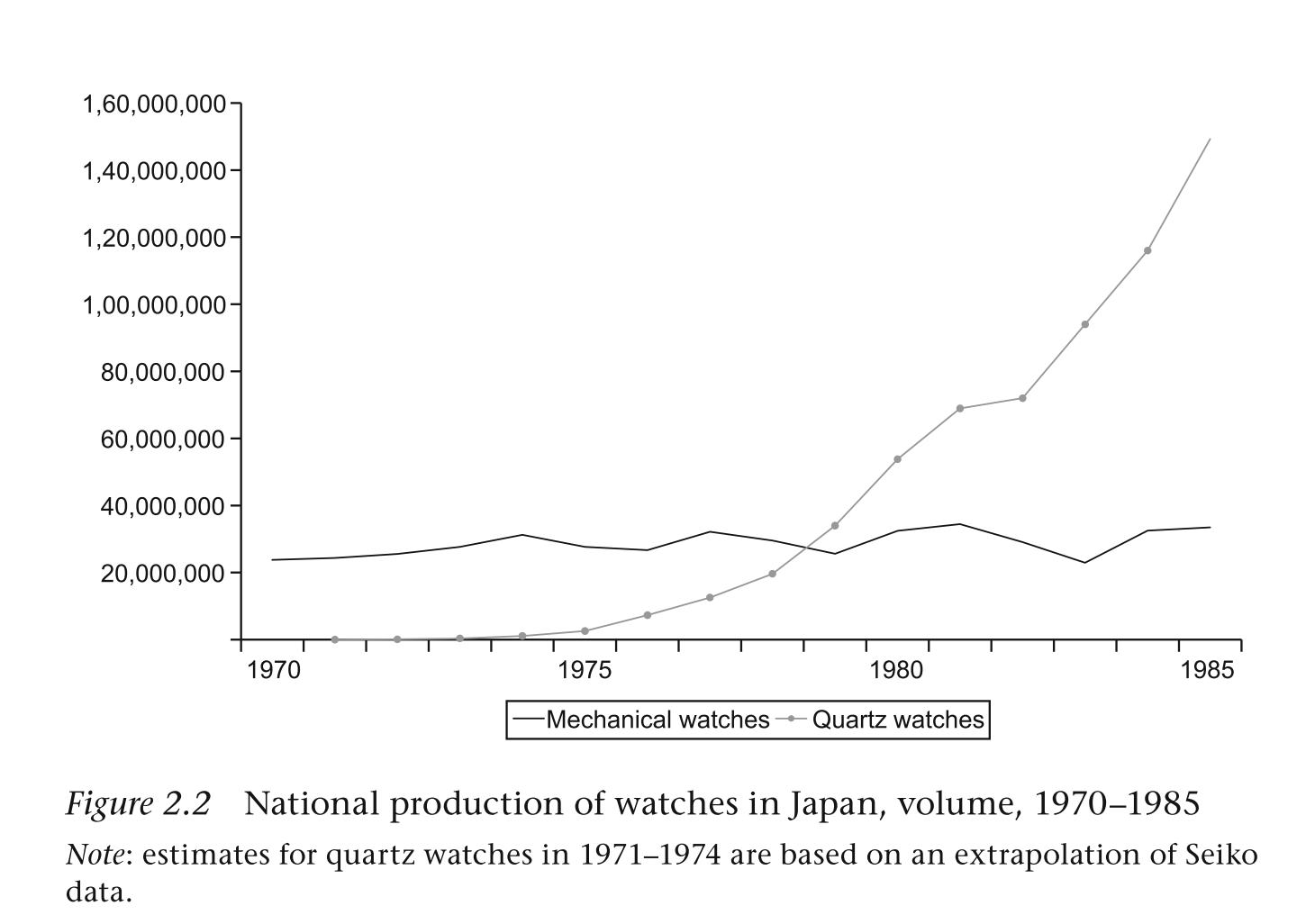

The second graph shows Japanese production of both mechanical and quartz watches from 1970 to 1985. Japanese mechanical watches were produced at a steady rate from 1970 to 1985 — 23.8 million pieces in 1970, and 25.6 million pieces in 1980. It peaked at 41.8 million pieces in 1986. The line looks like a flat wiggle across the decade.

The growth of Japanese quartz watch production, by comparison, looks like a hockey stick. But it really only takes off in 1979. In 1975, when Swiss exports started their dizzying nosedive, quartz watch production amounted to only 2.6 million pieces, or 8.5% of the total amount of Japanese watches produced. It took Seiko four years to perfect the technology (as we’ll see in the next section), and to bring down the price of the average quartz watch from the price of a small car to the price of a calculator. In 1979, four years later, quartz watches finally overtook Japanese mechanical watch production, at 33.9 million pieces, or 57% of total volume.

Combined, these two graphs tell a very different story from the mainstream Quartz Crisis narrative. In his 2014 book A Business History of the Swatch Group, Donzé writes (all emphasis added):

As a conclusion, it must be admitted that the real shift towards quartz watches occurred in Japan after the crisis had begun in Switzerland. The 1975 drop in Swiss watch exports cannot be directly linked to the quartz revolution — even if it reinforced Japan’s competitive advantage in the early 1980s — and the crisis in Switzerland.

Quartz did not cause the crisis. It merely accelerated what was already happening.

So what caused the crisis? Donzé turns to two things: first, the structure of the Swiss watch industry that we covered in the previous section. Second, the collapse of the Bretton Woods system in 1971, which caused the Swiss franc to appreciate against the US dollar. This in turn led to increased prices of Swiss watches in the US, its most important foreign market.

Of the two, the first was the bigger problem. The Statut horologer was abandoned in 1971, but for years afterwards the Swiss industry remained fractured. As an example, Omega, Tissot and Lemania had combined to form SSIH in 1930, but as was the case during that period, none of them shared movements or parts.

To make things worse, many of the high-end manufactures spread themselves thin across multiple market segments. At the end of the 19th century, the bottom end of the watch industry consisted mostly of pin-lever watches, also called ‘roskopf’ watches. These were cheap mechanical timepieces that used a pin-pallet escapement, as opposed to the lever escapement found in practically all high-end mechanical movements. Pin-pallet escapements were easier to manufacture, had looser tolerances, kept lousier time and were hard wearing — meaning they wore out quicker and were more likely to randomly break down.

It’s difficult to imagine this today, of course, because roskopf watches are completely obsolete. But back in the late 60s and early 70s, roskopfs made up the bulk of the Swiss watch industry’s output. They were crap. They were so cheap that they were deemed unworthy of repair; you threw them away once they broke down.

Many of the top Swiss manufactures expanded to pin-lever watches in addition to their high-end models. Omega was particularly bad. In 1970, acting on the recommendations of the McKinsey consulting firm, SSIH’s board brought in Pierre Waltz, a tobacco exec of some repute. He took a look at Omega’s product line up, from pin-lever watches to high-end chronometers, and decided on a strategy of rapid expansion: expansion, that is, to as many models in the cheapest end of the market.

Consequently, Omega spat out shitty pin-lever watches by the millions. From 1965 to 1974, the volume of watches that Omega sold soared from 3.4 million pieces to 12.5 million pieces. In 1973, 69.6% of SSIH’s sales volume were pin-lever watches, despite making up only 18.9% of their revenue (SSIH was Omega’s parent company, so this likely included pin-lever watches from Tissot and others). But it was undeniable that the strategy worked, for a while: from 1965 to 1974, Omega went from CHF245 million in revenue to CHF733 million. By 1980, Omega had 1,600 different watch models. Most of them were at the bottom end of the market.

To say that this dented the brand is a bit of an understatement.

By comparison, Seiko applied mass production techniques to high-quality mechanical watches. As early as 1949, Seiko’s production volume overtook Omega’s. By the time the 60s rolled around, Seiko was producing 3.7 million mechanical watches in 1960, and then 14 million in 1970. Unlike Omega’s strategy of filling the market with cheap roskopfs, Seiko gave the common man value for money: they produced a limited number of models that were specially adapted for mass production. Seiko watches weren’t the cheapest models on the market, though Seiko’s significant scale economies drove down prices over time. Between 1945 and 1967, Seiko sold only 123 mechanical models, as opposed to Omega’s several hundred. In 1967 and then 1968 the Japanese company won competitions at the observatories of Neuchâtel and Geneva, proving that mass produced Japanese movements could be just as accurate as the top Swiss chronometers.

More importantly, Seiko could execute a ‘highly rational marketing strategy organised on a global scale’. It had fewer models, which meant a higher-density sales network, targeted to a specific market segment. And it could do mass advertising, because — again — it had fewer models to do marketing for.

So it was no wonder that by the time the 70s rolled around, Japanese mechanical watches were eating the Swiss watchmakers' lunch. The bulk of the Swiss industry’s output was crappy pin-levers; these roskopfs were being displaced by higher quality Japanese mechanicals at a fair (but constantly declining) price. When Seiko finally got quartz to work, the roskopfs were pretty much wiped off the market.

Quartz

The story of the quartz movement begins more than a hundred years before the ‘Quartz Crisis’.

Traditional mechanical watches use a series of miniature gears, springs, and other components that work in conjunction to measure the passage of time. The mainspring provides the power, the gear train transfers the force, the escapement regulates the movement, and so on. Aled Maclean-Jones puts it beautifully in his piece, Watch men:

It’s an intricate system which evolved over centuries, but one that ultimately involves tiny physical objects bumping up against other physical objects – something that hasn’t really changed since the earliest documented mechanical clocks were installed in the fourteenth century in cathedrals such as St Albans, Norwich, Salisbury, and Wells.

For hundreds of years, mechanical timepieces were the “gold standard” of timekeeping. The techniques invented in those early decades are still used today. However, in 1880, without realizing exactly what it meant, French scientists Pierre and Jacques Curie uncovered something that would alter the course of timekeeping forever. While studying the impact of mechanical stress on crystalline materials, the brothers discovered that when an electric charge was applied to quartz, the mineral vibrated at an extremely precise frequency. This phenomenon was dubbed the piezoelectric effect.

In the ensuing decades, the Curie brothers’ discovery was relegated to laboratory settings. That changed during World War I, when French physicist Paul Langevin used piezoelectric quartz transducers to develop the predecessor to sonar. Langevin’s experiments showed quartz crystals stimulated by an electric current produced sound waves that reflected off submarines and returned to a detector.

From there, it was a short conceptual step to use quartz oscillation for timekeeping. If a quartz crystal vibrates at a precise, consistent frequency when electrically charged, it can certainly serve as a time reference. This notion was proven correct in 1927, when researchers at Bell Telephone Laboratories in New York constructed a massive quartz clock.

For years, quartz clocks were used in broadcasting centers and telecommunications stations, where precise time measurement was critical. It wasn’t until 1967 that a quartz wristwatch was made. Ironically, this new technology was developed by a consortium of Swiss enterprises at the Centre Électronique Horloger in Neuchâtel. Here, researchers designed and built the Beta 21, an analog quartz movement used by Swiss brands such as Omega, Longines, and even Rolex for a short time.

The quartz watch was, by almost every measure, a superior timekeeping machine. Using a battery to pass an electrical charge through a quartz movement, this new wristwatch could keep time more precisely than a mechanical wristwatch by orders of magnitude. Plus, it needed fewer parts and required less labor. But despite all this, Swiss watchmakers walked away from the technology they had just invented.

Why they did so is interesting to consider. Early histories of the crisis argue that Swiss watchmakers were stubborn, or complacent. One early historian of the Swiss watch industry, Harvard professor David Landes, pinned the problem on a lack of ‘dynamic entrepreneurship’ amongst family-owned Swiss firms, due to years of sheltered rent-seeking. Others argued that quartz threatened their margins, or violated their craft identity. Perhaps quartz only attacked the low end of the market, which the Swiss watchmakers were not interested in. But none of these are likely to be correct. Many manufactures were already producing cheap, low margin roskopfs by the container-load in the 70s. Second, a ‘lack of dynamic entrepreneurship’ is a symptom, not a true cause.

Donzé believes the real problem was structural. Thanks to the Statut, there was a lack of rationalisation in the production systems of the entire Swiss watch industry. Quartz started out as an exceedingly expensive technology. You needed scale economies — and learning economies — to bring the costs down. In terms of structure and incentives, the Swiss watch industry simply wasn’t set up for that. And even if it were — even if a small group of firms were committed to reorganisation in order to pursue quartz technology — they would still have to reckon with the Japanese, who were already set up for mass production.

This set the stage for what occurred next. Seiko released the first commercially available quartz wristwatch on Christmas Day 1969. Known as the Astron, the elegant timepiece retailed for $1,250 ($11,342 in 2026 dollars) and was 100 times more accurate than anything else available at the time. But $1,250 was basically the price of a Toyota Corolla at the time, which meant the Astron was undoubtedly a luxury watch.

Seiko was committed to driving down its production costs. In many ways Seiko’s corporate identity was — and still is — built around continuous innovation. It redirected much of its engineering resources and manufacturing capacity towards this new quartz technology. By 1979, Seiko had slashed the Astron’s power draw from 30 microwatts to three microwatts, slimmed its movement thickness from more than five millimetres to under one millimetre, and cut its retail price to 2-3% of its initial price, or about $25-$37.50 ($114-$172 in 2026 dollars). During that time, Seiko also added new features to its flagship product, including calendars, calculators, stopwatches, and alarms. Aled Maclean-Jones writes:

Even worse for the Swiss, Seiko licensed its key quartz patents to other makers, a strategic move aimed at setting global standards, accelerating adoption and cementing Seiko’s lead. The result was a flood of Japanese competitors, most notably Citizen and Casio, both of which launched their first quartz watches in 1974. Buoyed by extremely favorable exchange rates, Japanese watch production tripled during the 1970s, soaring from just under 24 million units in 1970 to nearly 90 million by decade’s end.

Competition was fierce in Japan. Seiko, Citizen, and Casio sparred over the global quartz watch market. The environment drove innovation, which sparked industry-wide improvements at a stunning rate. Seiko was vertically integrated from the beginning. It manufactured its own cases, grew its own quartz crystals, and made its own batteries, thereby facilitating control over its entire supply chain. This allowed it to streamline designs at a rapid rate, and when it scaled up production volume, gave it an edge that few competitors could match. Still, other Japanese watchmakers attempted to follow in Seiko’s footsteps. This made it doubly difficult for Swiss manufacturers to keep up.

Between 1970 and 1980, the overall value of Japanese watch companies’ production soared from $350 million to $2.0 billion. In 1977, Seiko generated more revenue than any other watch company in the world, and in 1980, Japan officially became the planet’s largest watch producer. Analysts everywhere were writing obituaries for the Swiss watch industry. As economic historian Landes put it:

The quartz timekeeper is a superior instrument in terms of both precision and price, and is bound to win out. Here we have a rare opportunity to study the birth, maturity, and obsolescence of a major branch of manufacture.

Emboldened, Seiko released an advertisement that read: “Someday all watches will be made this way.” They weren’t wrong, at least not in the short term. Between 1981 and 1985, the average value of Japanese watch production was $1.96 billion, outpacing the $1.69 billion average for Swiss exports (Switzerland’s domestic market was negligible).

It was at this point that Nicolas Hayek stepped into the picture.

Hayek’s Vision

Nicolas Hayek was born in Lebanon in 1928, but he had adopted Switzerland as his home.

After studying math, chemistry, and physics at France’s Lyon University, Hayek took a job as an actuary at Swiss Re, a leading provider of insurance and reinsurance. By 1963, he was ready to leave. To secure startup capital for his new consultancy, Hayek took out a bank loan and famously pawned his household furniture.

Hayek’s calculated risk would pay off. Over the next few decades, his Zurich-based consulting company, Hayek Engineering, became a great success. He specialised in management, manufacturing, and supply chain issues. By the 80s, Hayek Engineering had built enough of a reputation for itself that it was described as: “a cross between Arthur D. Little and McKinsey & Company.”

Seeking an offramp, in 1982, a group of Swiss lenders hired Hayek to advise on a potential sale of SSIH and ASUAG. For the bankers, it was evident that the Swiss watchmaking conglomerates were in their death throes. But Hayek, who hadn’t worked on a watch a day in his life, thought otherwise.

To understand why this might be the case, imagine, for a moment, that you are Nicholas Hayek. You have spent 25 years of your life working on production issues in industrial companies. Previously you saved the German steel and metalworking industry — where rationalisation of the means of production was a crucial issue. In that case, you combined the assets of multiple firms (AEG, Krupp, Mercedes and Volkswagen) and you solved the industry’s problems in one fell swoop.

At first glance, the Swiss watchmaking industry looked much the same.

And so rather than liquidating, Hayek proposed merging ASUAG, which specialised in movement production, and SSIH, which held some of the top Swiss brands. This new company would be called the Swiss Corporation for Microelectronics and Watchmaking, or SMH. And though many insiders thought Hayek was nuts, the engineer-consultant had done his homework.

In his words, he had found: “A chaotic jungle. An absolute mess.” But within that mess, Hayek had discovered many usable parts.

ASUAG owned a mix of small, medium, and large companies, each conducting its own R&D, marketing, and assembly. It was muddled. But among ASUAG’s assets was Ebauches SA, later renamed ETA SA, the sole manufacturer for exportable movement blanks and Swiss watch movements. As an effective monopoly, ETA SA had the capacity to produce high-quality movements and components at a high volume. Hayek could work with this. He could shut down or consolidate various other departments or factories that did essentially the same thing. On the other side of the merger, Hayek found a portfolio of struggling but storied brands within SSIH that he believed could be restored to their former glory.

Passing this information along to the creditors, Hayek proposed salvaging the Swiss watchmaking giants. In 1983, the banks reversed course and accepted his core proposal. SSIH and ASUAG would merge into one entity. Hayek would take on a role as an advisor to the newly-created four-member Executive Management Board. This board oversaw the rationalisation of SMH’s production systems. And in this Hayek was in his element.

Within a single year, SMH managed to turn a small profit through rationalisation activities alone. The reorganisation of this new company took around four years to complete, from 1983 to 1987 or so. On Hayek’s recommendation, SMH created three sub-holding groups: ‘complete watches’; ‘movements and parts’; and ‘others’. Over the next few years, they closed all of Omega’s movement blank factories, and then Longines and Rado’s movement factories, and moved staff over to ETA. They also invested a significant amount of capital to upgrade production facilities.

In 1985, Hayek raised money with a group of wealthy Swiss German investors in order to buy a controlling stake in SMH. The most notable of these investors included Esther Grether and Stephan Schmidheiny. This was the point where Hayek was truly in charge of the management of the new company. His board was still filled with bankers, but he had operational control, and more importantly he was committed for the long haul.

While rationalisation could put SMH in the black, it had a profit margin of less than 5% of gross sales. Gross sales also grew slowly for the rest of the 80s. Hayek needed a growth strategy to truly turn SMH around. What could he do?

In the medium term SMH could increase its top line by selling Swiss-made watch movements to other companies, including those outside of Switzerland. Since it started from a monopoly position with such parts, it was perfectly happy to do so.

It could also increase profits by moving certain parts manufacturing outside of Switzerland. This second strategy was little known, and the result of a loophole: it was enabled by the fact that the ‘Swiss-made’ label only required 50% of components to be made within Switzerland. Historian Donzé takes great pains in his A Business History of the Swatch Group to detail the various Asian subsidiaries that SMH quietly set up outside of Switzerland in the late 80s and 90s, in order to drive costs down. This occurred as early as 1985, when SMH set up a factory in China. (It moved it to Thailand the following year due to difficulties with the Chinese government.)

Both of these moves — exporting Swiss movements as well as quietly moving parts production out of Switzerland — were straightforward things to do. And of course the group did them. But they were not emphasised in any of the official histories of the Swatch group. Hayek still wanted a major source of growth — something that could take the fight to the Japanese.

Years later, Hayek would describe the competitive environment as a “three-layer wedding cake” which he believed was ripe for the picking. As he said:

Back then, the world market for watches was about 500 million units per year. The low-end segment, the bottom layer of the cake, had watches with prices up to $75 or so. That layer represented 450 million units out of 500 million. The middle layer, with watches up to $400 or so, represented about 42 million units. That left 8 million watches for the top layer, with prices from $400 into the millions of dollars.

The Swiss share of the bottom layer, 450 million watches, was zero. We had nothing left. Our share of the middle layer was about 3%. Our share of the top layer was 97%.

Hayek wanted something to tackle the bottom layer. And he wanted it done in Switzerland. But to do that, he needed to bring his production costs down in one of the world’s most expensive countries. Hayek stated: “If we can design a manufacturing process in which direct labor accounts for less than 10% of total costs, there is nothing to stop us from building a product in Switzerland.” When SMH was formed, direct labor accounted for approximately 30% of the company’s costs. By the time Hayek was finished, they would be well below his 10% target. As Hayek told business journalist William Taylor: “If we paid our workers full salaries and the Japanese paid their workers nothing, we could still compete.” (He left out the part where he was moving the production of certain parts to Asia).

A supply-chain specialist, Hayek had little experience with watchmaking. The consultant wasn’t a craftsman; he had no feel for the artistic side of the business and no attachment to what could be lost. It would take more than just Hayek’s engineering expertise to get the industry back on track. He needed a marketable product.

As it turned out, that product was already being built by two engineers in a factory in Grenchen, without anyone’s permission. Hayek found the product in the bowels of his company.

And then he built an entire strategy around it.

The Engineering Miracle

Elmar Mock was a watchmaking engineer in 1980, working at ETA. The ASUAG movement-manufacturing subsidiary had been the first Swiss company to mass-produce quartz movement blanks in 1979.

That same year, ETA engineers built what at the time was the world’s thinnest watch, the Delirium. Measuring just 1.98mm thick, this marvel of Swiss ingenuity was a ray of light in an otherwise depressing corporate environment. However, the piece retailed for $5,000 ($22,935 in 2026 dollars). It was too expensive to stem the decline of the Swiss watchmaking industry.

With potential liquidation looming, ETA began laying off employees at a rapid pace, firing over 4,000 in one year. Mock and his colleagues all feared they would be the next to get the axe. And so Mock had little left to lose. As he recounted: “My first dream wasn’t to make a watch. It was to have an injection moulding machine.”

From the Swiss perspective, injection moulding offered a radical alternative approach to watchmaking. Rather than using brass, steel, or gold and then cutting, pressing, and polishing, this system used plastic to produce a watch case in a single step.

The problem? An injection moulding machine cost 500,000 Swiss francs, or approximately $300,000 at the time.

And Mock had the authority to spend exactly zero of that.

However, in a bout of desperation, he ordered the machine anyway. That same day, Mock received a call from his general manager, Ernst Thomke, requesting that the engineer be present in Thomke’s office in about two hours. Mock knew what that meant. But instead of preparing his apology and begging for his job, he ran to meet his colleague, Jacques Müller.

Müller and Mock had spent the previous month brainstorming concepts for a new watch. They envisioned something entirely different from the traditional options that Swiss manufacturers were known for. With little time before the meeting, the pair sketched out their idea, which Mock called: “a childlike pink and blue quartz model made of plastic.”

For the first 30 minutes of Mock’s meeting with Thomke, the general manager tore into his subordinate. Irate, Thomke wanted to know who would be crazy enough to spend $300,000 on an unauthorized piece of machinery, especially one that wasn’t even applicable to Swiss watchmaking.

Once the undressing ended, Mock pulled out his blueprint for a colorful quartz wristwatch. Thomke was intrigued. He told Mock that he had been hoping to manufacture a cheap Swiss quartz for mass production. He gave Mock and Müller six months. It took them 15 months to come up with a prototype. As 1980 came to a close, they had completed five watches, but each one stopped ticking after only five days. That would soon change.

Building off of the technology their fellow engineers used to craft the ultra-thin Delirium, Mock and Müller focused on making something small, simple, and, most importantly, cheap. Their innovation was using ultrasonic welding. This allowed them to build the mechanism directly into the plastic case, nearly halving the standard number of parts in a quartz watch, down from 91 to 51. The result was a timepiece that was three times cheaper to produce than any other watch made in Switzerland at the time.

Mock and Müller’s fun little watch was initially called the Vulgaris. It would later become known as the Swatch. The Swatch’s design was innovative, but a lot of things had to go right for it to win. SMH nailed the Swatch’s production process. As Nicolas Hayek explained:

When we designed the Swatch factory, we built special machines for injection molding, automated assembly—virtually everything. There were only a handful of people in the world with the know-how to build those machines. They all lived in this part of Switzerland.

Soon, the SMH factory in Grenchen was producing 35,000 Swatches a day, in addition to millions of components. Each night for eight hours, the facility operated with virtually no human input. This bore Hayek’s fingerprints. Mock reflected on what he and Müller’s design had set in motion:

My first production target was 50,000 watches. Swatch has now sold more than 700 million. Has it made me rich? Well, a year after the product went on sale, I got 700 Swiss francs as a thank you bonus.

Though Mock may have felt he was undercompensated, his watch design, combined with Hayek’s supply-side work, had put the Swatch in a position to change the course of Swiss industry. But the work wasn’t finished yet.

The Message

For all of the innovation involved in creating the Swatch, it was still just another quartz watch in a sea of affordable quartz watches. By the early 1980s, Japan and Hong Kong had flooded the market with hundreds of millions of cheap quartz timepieces.

What would set the Swatch apart from its competitors wasn’t its price. It was its Swiss identity. In other words, its emotional appeal, characterised by Swiss quality, Swiss culture, and the Swiss joie de vivre (joy of life). To evoke these sensations, the marketing team dropped the Swatch's original name, “Vulgaris,” which is Latin for “ordinary.” For Hayek and his team at SMH, the Swatch was anything but ordinary.

The name was changed to “Swatch,” a moniker developed by marketing specialist Franz Sprecher, who combined “Swiss” and “watch.” According to Sprecher: “It wasn’t sexy but we knew that, although Switzerland had lost a lot of momentum to the Japanese, anyone who owned a Japanese watch would still pretend to have a Swiss one.”

SMH launched the Swatch for $40 at Bloomingdale’s and other upscale American department stores. This was in contrast to Japanese quartz watches that sold for $10 in corner drugstores. At Hayek’s directive, the company invested 25% of Swatch’s total budget in marketing, an unheard-of move in the industry at the time.

The brand’s positioning was seen as radical. But much about the Swatch’s marketing strategy was deliberate. Other watches in the same market segment were positioned as simple, functional objects, and nothing more. They were accurate, reliable, and affordable, but they were definitely not “cool.” The Swatch aimed for cool. As Hayek stated:

We are not just offering people a style. We are offering them a message. This is an absolutely critical point. Fashion is about image. Emotional products are about message — a strong, exciting, distinct, authentic message that tells people who you are and why you do what you do.

The Swatch was bright and rebellious. It broke sartorial rules with class and sophistication. It didn’t ask for permission and didn’t apologize for standing out. During Swatch launches in Germany, Japan, and Spain, SMH draped giant 165-meter-long replicas from the countries’ most prominent skyscrapers. To celebrate the first million Swatches sold, Hayek convinced Commerzbank to let him hang a 13-ton Swatch replica from the German institution’s Frankfurt headquarters, remembering:

It was a big provocation to hang a watch from a huge, grim skyscraper. And it was funny, fanciful, a joke — joy of life. Believe me, when we took it down, everyone we had wanted to reach had received our message.

Hayek’s company embraced pop culture, associating the Swatch brand with youthful activities such as skateboarding, snowboarding, and breakdancing, even hosting a breakdancing competition in 1984. It backed independent musicians, trendy fashion events, and alternative art exhibitions, collaborating with acclaimed street artist Keith Haring, whose Swatch designs became prized collectibles.

When things didn’t go to plan, Hayek and company leveraged the circumstances to their advantage. Due to Mock and Müller’s unconventional design, the Swatch transmitted vibrations through its case, something other quartz watches did not. This triggered an audible ticking sound, which many consumers found annoying.

According to Franz Sprecher, customers complained at first: “Oh, they’ve made a watch that ticks! And you cannot sleep! And in a concert, everybody hears it!” In a stroke of marketing genius, Swatch flipped those complaints on their head by releasing an advertisement that read: “It’s only Swatch that ticks.”

People loved it. Among young professionals, known as “yuppies” at the time, the Swatch was a major hit. Whenever an upscale department store released a new Swatch, lines would form outside the door hours before opening. As Sprecher recalled: “I remember standing in The Plaza hotel in New York and noticing that all the yuppies were wearing Swatches. It was a statement: ‘I don’t need a Rolex.’”

For many, it wasn’t necessarily that they couldn’t afford a Rolex; it was more about making the statement that they didn’t need a Rolex. Well-known designers and artists competed to put their mark on new Swatch releases. To them, the Swatch was a blank canvas that offered a path to hipness and a one-way ticket to notoriety.

For anyone paying attention, it became clear that the little Swiss-made quartz watch had become a cultural icon. By 1988, SMH produced and sold 50 million Swatches. In 2010, that number would exceed 700 million. But Swatch’s significance went beyond its sales figures. In official communications, Hayek argued that the cheap watch and the expensive watch weren’t competing strategies. They were, in Hayek’s view, complementary:

I really believe the phenomenal success of these $40 watches helps the climate for selling $500 watches—or $5,000 watches, for that matter. We have reestablished our technical superiority over the Japanese watchmakers. If we can build beautiful, high-quality watches that sell for only $40, imagine what must be the quality and accuracy of watches that sell for $2,000!

In the popular narratives encouraged by the Swatch Group, the success of the Swatch provided the cash that Hayek could use to acquire and rehabilitate its older, higher-end Swiss watch brands.

This is not entirely without merit, but it is overstated. In truth, Swatch was only truly hot for about 10 years after its launch. In his history of the group, Donzé puts together evidence from Swiss export data to argue that SMH profits from Swatch sales were likely only a minor part of SMH’s overall profits after 1993. (Specifically, Swatch peaked at nearly 30% of overall gross sales in 1993, before falling to 5% in 2000, where it has held steady since. Note that these are estimates; Donzé does not have access to group sales data). Donzé then argues that while Swatch did contribute cash for the restructuring in the early phase of Hayek’s leadership, what was more important about the Swatch experience was what Hayek and his executives learnt from growing the brand.

What they learnt was globalised, standardised marketing. Before the Swatch, it was not clear that you could create (and sell!) a global brand that was not adapted to local markets. Experience growing the Swatch brand, as a fashion product, showed SMH that globalisation in end consumer markets was a thing: you could create a cultural product that was marketed in exactly the same way across the world. Donzé writes:

Until the 1980s, Swiss watch brands followed a great many different approaches worldwide. Many watch manufacturers exported only naked movements (44 per cent of the total volume of watch exports in 1980), 16 which were encased in Hong Kong or the main markets on which they were sold. This strategy provided a means of cutting production costs, which were high in Switzerland, and offering consumers products that matched local tastes. The design, functions, price, communication, and image attached to brands often varied considerably from one country to another, to such an extent that one cannot speak of a “global brand” during this period. Consequently, the Swatch marked a real break in this field.

Hayek had stemmed the red at SMH and created a successful consumer brand at the lower end of the market. That successful new brand generated some of the cash that allowed SMH to pay down its considerable debt and to restructure its operations successfully. The next stage of the turnaround, however, required what Donzé calls ‘marketing-driven rationalisation’ — connecting all the advances in production rationalisation to a coherent marketing strategy.

This next phase was driven by a completely different man.

Biver’s Bet

Despite the overwhelming trends of the 1970s, not everyone believed that quartz was the inevitable future of watchmaking.

Jean-Claude Biver, a former Omega product manager, was among the most ardent contrarians. Biver had spent the early years of the crisis managing Omega’s gold-watch collection, affording him a front-row seat to the complacency and strategic confusion that led to the firm’s shocking decline.

Biver knew that Omega’s parent company, SSIH, was clinging to life. The once-proud Swiss watchmaking institution was nearly bankrupt and willing to sell off its dormant assets for pennies on the dollar.

Omega was SSIH’s “crown jewel.” In its heyday, it competed toe-to-toe with Rolex. Omega’s most famous timepiece, The Speedmaster, was the watch worn by astronauts Neil Armstrong and Buzz Aldrin during their 1969 moon landing, having been the only wristwatch to pass NASA’s rigorous testing program. Now the entire brand was on the brink of death.

Thanks to a strategic mistake by former head Pierre Waltz, Omega was spread extremely thin. It was still locked into the ‘let’s sell as many models as possible’ direction that Waltz had chosen. As quartz ate up the bottom of the market, Omega had expanded to sell (many) new quartz models, also at the bottom end of the market. This did not work. As Nicolas Hayek later told William Taylor, the former associate editor of Harvard Business Review:

Omega was everywhere: high price, medium price, precious metals, cheap gold plating. There were 2,000 different models! No one knew what Omega stood for. By the end of 1980, the company was again in a deep crisis, its deepest ever.

Omega’s downward spiral left a lasting impression on Biver. He had developed strong opinions based on what he had seen. So his plan for the path forward was straightforward. According to Works in Progress, Biver believed in his bones that: “Swiss watchmaking could survive only by rejecting quartz and doubling down on high-end, handmade mechanical watches.”

Acting on this instinct, Biver partnered with Jacques Piguet, the CEO of movement manufacturer Frédéric Piguet SA. In order to test Biver’s ideas, the pair needed to gain control of a prestigious Swiss watch brand. They eventually settled on the storied watchmaker Blancpain.

Among the oldest and most respected brands in Switzerland, Blancpain had first joined SSIH in 1961 via a subsidiary called Rayville. After selling 200,000 watches in 1971, Blancpain spent the rest of the 70s in decline. At the start of the 80s, it was all but forgotten. That allowed Biver and Piguet to acquire the company in 1981 for the paltry sum of 16,000 Swiss francs, or about $9,000.

The pair got to work rehabilitating the brand. Operating out of a farmhouse in the Swiss mountains, they employed out-of-work watchmakers whose livelihood had been destroyed by quartz. Thanks to his role as CEO of a movement manufacturer, Piguet had connections to old, family-run artisanal houses, which meant access to high-quality, mechanical movements at a time when the infrastructure for making them was rapidly disappearing. Biver brought commercial instinct, marketing chops, and vision. In a world where mechanization was taking over, he planned to establish Blancpain as a global leader in handmade, craftsmen-led, artisanal watches, leading with the slogan: “Since 1735, there has never been a quartz Blancpain watch. And there never will be.”

It’s difficult to underscore how differentiated Biver’s pitch was at the time. Before the pair gained control of Blancpain, many timepiece brands were primarily marketed as tools. (Yes, even Rolex’s watches were initially marketed as ‘tool watches’). Biver’s pitch was thus genuinely new, and it was emotional at its core. Biver sought to treat the watch as an artistic object, with utility as an afterthought. Scarcity was central to his plan. As he noted: “We wanted to be very exclusive.” Furthering his brand’s artisanal image, Biver personally hand-delivered watches in the early days, explaining to his customers how hours of intricate work had gone into each piece. In the first year of Biver and Piguet’s stewardship, Blancpain sold 97 watches, amassing $75,000 in revenue.

Biver and Piguet traveled to the Basel fair together in 1984, then the world’s most important annual trade show for the watch and jewelry industry. In order to save cash, the duo slept in their Volkswagen Westfalia, waking up early to wash in train-station restrooms before setting up shop inside the Basel Exhibition Center.

At the time, Blancpain had only two watch models. Biver and Piguet chose to leave both display cases empty. The stunt aroused curiosity. It made for a strange scene: a booth for a storied brand, in the hands of a pair of young men, with no products, juxtaposed against the globe’s top watchmakers and jewelers unveiling their newest lines. Biver and Piguet had the chance to opine on their favorite topic — pitching potential customers on the merits of Swiss watchmaking while highlighting the value of mechanical watches. One veteran of the watchmaking industry remembered:

In 1982 there was literally no market for mechanical watches. And then Jean-Claude comes along and represents this crazy belief that mechanicals had a future. He was a visionary to see the old world was still important. He offered up a symbolic point of view that brought back the artistry and the tradition.

Within five years of purchasing Blancpain, Biver and Piguet were selling 3,000 watches a year and reporting $9.4 million in annual revenue. Biver’s unorthodox strategy had worked. He had taken a company that had lost all of its value and completely revitalized its image. In doing so, he and Piguet proved that there was still a sizable, albeit niche, market for handmade mechanical luxury watches. In 1992, they sold Blancpain to SMH for $43 million.

Nearly immediately, Hayek recognised what he had with Biver.

{kind=link}

The Pursuit of Affordable Luxury

Other things were afoot within SMH when Hayek acquired Blancpain. First, it had spent the late 80s consolidating distribution. SMH had multiple sales offices in many countries. For instance, they had five in Germany (Certina, Endura, Longines, Omega and Rado). From 1985 onwards, the company made it a policy to have only one sales office per country, managing multiple brands. This was, after all, the logical thing to do. The savings from closing up the redundant sales offices were used to set up new offices in new countries, so it wasn’t really a cost-saving move (the total spent on fixed assets dedicated to sales netted out to around even).

But there were other, production related benefits to this rationalisation. The biggest one was to rationalise logistics. Here again Hayek showed his colours as a supply chain specialist: in 1985, inventory of watches and parts were a major financial burden for the company; they represented 33.6% of the balance sheet. By 1995 the share had fallen to 25%.

But the most important outcome of this rationalisation was that it laid the foundation for Biver’s strategy. It was not clear that Hayek knew how important this was when he started consolidating distribution. But by the start of the 90s, given his experience with Swatch, it was becoming clear that the only way to control the image of your high-end watch brands is to have direct control of individual markets. It is easier to standardise product image across brands if you had only one sales office per country.

There was one other move that Hayek did that paved the way for Biver’s eventual impact on SMH. In 1990, Hayek reorganised operational management at the top of SMH to focus on brand management and marketing. Many of the leaders who helped with SMH’s production rationalisation left the company. In particular, Ernst Thomke, who was critical to the creation of Swatch and the production restructuring throughout the group, left after a falling out with Hayek. He was followed by a number of his close business partners.

Hayek established a new Extended Group Management Board, which consisted of the managers of each of the watch brands. This would be his brain trust. Biver would be added to this group in 1992, when SMH bought Blancpain, and would be one of its most important executives. But the board had already started acting before Biver joined.

How do you make a lot of money in luxury? You might think that the answer is to concentrate at the tippy-top of the market: small volume, artisanal products sold at astronomical prices, executed at the highest possible levels of craftsmanship and quality.

You would be wrong.

The key to making a lot of money in luxury is to own an affordable luxury brand. This is in contrast to an ‘exclusive luxury’ brand. Affordable luxury is something that can be sold at an aspirational price point, slightly out of reach of the middle class. These goods should have high margins, but be mass produced at volume so that you enjoy economies of scale, and therefore generate large amounts of absolute dollars.

To use a watch world example, Patek Phillippe sits near the top of the luxury pyramid. It uses the most expensive materials (gold, platinum, titanium), with the best craftsmanship (unique enamel artwork hand-painted and fired by artisans), producing complex, handmade watch movements (e.g. movements with moonphase dials, as an example) and with a small total output of timepieces a year (around 62,000, by most estimates). The cheapest Patek costs in the tens of thousands of dollars. It is not mass produced. By contrast, Rolex makes between 800,000 to a million watches a year, at a lower price point. And this makes sense: a young professional could save for a few months (as opposed to a few years) to buy a Rolex. Because Rolex uses mass production techniques, their scale enables them to drive costs down, matching (or even exceeding) the profit margins of a Patek watch. But because Rolex sells more absolute watches at its lower prices, it generates far more cash than Patek ever will.

Rolex is affordable luxury. Patek Philippe is exclusive luxury. Both are good businesses. However, Rolex is what you want to own if you want to generate huge gobs of cash in the luxury business.

This is easy to say today, since the approach has been explicated in books and papers by luxury industry practitioners, often in partnership with academics. But back in the 90s this approach was still being developed. It was not widely understood. Folks such as Bernard Arnault at LVMH and then Johann Rupert at Richemont were putting together the dynamics of the luxury business throughout the 80s and 90s. Much of the tactical know-how to execute this strategy was still stuck in the heads of various brand managers within the industry.

It is difficult to say how Hayek stumbled onto this idea. After Hayek’s management reorganisation, SMH began to reposition its brands. Their first step was to differentiate the brands they already owned, so that none of them competed directly with each other. They repositioned Longines downwards, as it was too competitive with Omega. (Longines remained within the ‘affordable luxury’ price segment, but it was refocused on elegance and classicism, at a lower overall price point to Omega). They also took Tissot and positioned it much lower, in the middle of the market. They placed Rado in a niche around high technology materials (such as lanthanum and ceramics) and avant garde design. Critically, SMH deemphasised Rado and Longines in their group marketing in order to leave the high-end of the affordable luxury segment clear … for Omega.

As you might’ve already guessed, Omega was chosen to be the core affordable luxury brand — the cash cow of the entire group.

To this end, SMH began withdrawing from distributors that did not give its watch brands the attention or store space it desired. In the late 90s it began pursuing ‘flagship stores’ as a strategy, where SMH had ultimate control of product image and messaging. Most of this came from the learnings with Swatch, which originated the flagship stores strategy in 1996. Swatch was, after all, a fashion product, and the flagship store concept was borrowed from the fashion industry, where it was common to put single-brand stores on premium real estate in the major metropolises of the world. Each of these stores would have identical design and atmosphere, so that ‘the customer could live the brand’. Swatch copied this concept, and after proving it out — and showing Hayek that globalised brand marketing was now doable — the rest of SMH’s watch brands followed.

It was into this context that Biver joined SMH.

The Restoration of Omega

When Biver arrived in 1992, parts of this strategy were already in-flight. But they still needed an affordable luxury brand to anchor the strategy. The group had chosen Omega, but the problem was that Omega’s brand was still in the dumps. It needed to be rehabilitated. Hayek entrusted Biver with this critical task.

Early in his tenure, Biver switched Omega from image-driven advertising to a message-driven advertising model. Some slogans of the Biver era included “Omega — the link between the past and the future” (1994), “Omega — trust your judgment” (1995), and “Omega, my choice” (1997). This switch seems trivial, but it gave Biver the means to use the brand as a vehicle to tell a story. It is the creation of that story — and the usage of images to evoke emotions — that turns a watch into a luxury good.

In those early years, Omega’s marketing team had great leeway to tell specific stories within the constraints of the yearly slogans. Biver staged Omega’s comeback at the Basel Watch Fair in 1993. The team organised a ‘space forum’, with several famous astronauts in attendance. This was to remind attendees that Omega played a pivotal role in the American space program — it was more than a has-been! The next year (1994, the year of “Omega — the link between the past and the future”) Biver’s team caused a stir at Basel by inviting Neil Armstrong and launching a collection of Speedmasters watches to mark the 25th anniversary of the moon landing — the Speedmaster being the watch that Armstrong wore to the moon.

Biver then did three things in parallel: he reestablished Omega’s technical bonafides, he refocused a significant part of the brand’s messaging on Omega’s history, and he began associating the brand with glamour. Donzé uses the shorthand ‘technique, history, and glamour’ for this strategy, and this might just as well be a recipe for creating a luxury brand from scratch.

We shall tackle the three elements in order. Biver did a bunch of things to reestablish Omega’s technical legitimacy. The two most important were increasing Omega’s share of chronometer certifications, and second, adopting new technology to show that Omega was technically innovative.

Chronometers are watches that are certified by Contrôle officiel suisse des Chronomètres (COSC). Watchmakers submit timepieces to COSC for testing; if the piece passes a bunch of timekeeping tasks under rigorous simulated conditions, the timepiece would be awarded a chronometer rating certificate. This trend began in 1960, and for a few decades, Omega registered a large share of chronometers. Between 1961 and 1974, for instance, Omega registered 48.9% of all chronometer certifications, compared to 38.2% for Rolex. After 1974, as the crisis hit Omega, the number of Omega certifications fell from 190,396 pieces in 1974 to fewer than 30,000 pieces a year during the period of 1975 to 1984. Under SMH, production rationalisation led to a further deemphasis of chronometer registrations. Omega was awarded a mere 5,657 certifications a year from the years of 1985 to 1989.

This meant that for more than a decade, they had abandoned the entire category to Rolex, whose share of chronometer certifications leapt to 89.2%.

Biver immediately began to increase the number of chronometer registrations once he took over. Omega’s chronometers rose from 190,516 certificates in 1994 (12.7% of the total registered) to 342,798 certificates in 2010 (26.9%). Other watchmakers paid attention. Within a decade, other watch brands — amongst them Breitling, TAG Heuer and Panerai — began pursuing COSC certification to establish their technical bonafides, copying Biver’s strategy.

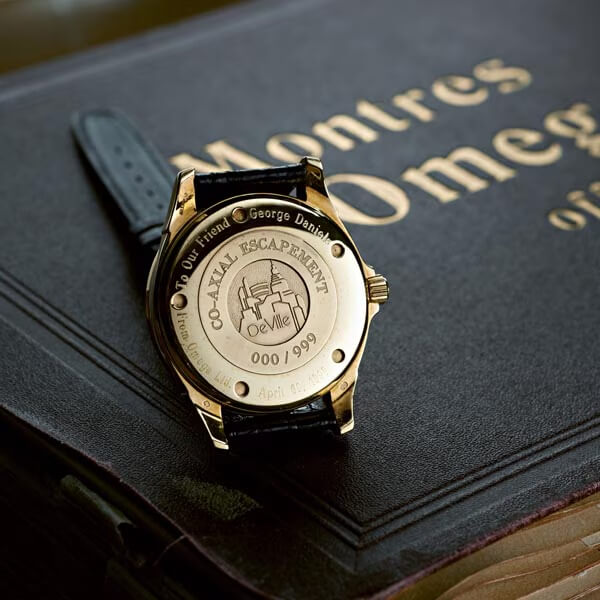

Biver also released a complicated tourbillon model in 1994, as if to prove that Omega still ‘had it’. Most importantly, however, in 1999 Omega released a watch with an ETA movement coupled with a new escapement called the ‘coaxial’ escapement. This escapement was invented by renowned British watchmaker George Daniels; SMH had bought the exclusive rights a few years earlier. The brand then released a new Omega-specific movement coupled with the coaxial escapement in 2007, and the escapement continues to be a major part of Omega movements today.

There are two interesting things about this story. The first is that the Omega-specific movement was made by ETA, not by Omega, because SMH had long reorganised itself to have all movement manufacturing occur centrally, within its ETA subsidiary. But no other brand in the SMH stable was allowed the coaxial movement. In order to establish Omega as the premier ‘affordable luxury’ brand, an exception was made to the principle of rationalised production.

The second interesting thing is how Biver approached the marketing of this new movement. The naive approach to technological innovation is to focus on the technical superiority of the technology. In theory, the coaxial escapement was superior to the mainstream lever escapement because it caused less friction, thus increasing reliability of the overall movement. Omega watches with coaxial escapements therefore needed to be serviced less than other mechanical watches. (Again, this was in theory — in practice servicing depends on many other factors, and is therefore more complicated than just “less friction, therefore less servicing”).

But Biver did not focus on the technology alone. Sure, he installed screens in all the Omega stores, playing videos of the escapement in action. But he used the escapement as a means to an end — and that end was to deliver the message that Omega had a grand history of technical innovation and excellence, and this was but a continuation of that grand history.

This was what Hayek had hired Biver for. Years later, Biver’s techniques would be explicated by business professor Jean-Noël Kapferer and former head of Louis Vuitton Vincent Bastien in their 2008 book The Luxury Strategy. Kapferer and Bastien argue that in a luxury product, technology “serves only to maintain the objective distance, but on condition that it keeps the dream: there is a potential for imagery and sublimation of the world running through the technology.”

A simpler way of putting this is that a luxury product is built around a dream — an aspirational desire evoked by storytelling. The customer is willing to pay an excessive amount above and beyond what they are getting in pure functionality. A premium product, on the other hand, is built around utility: ‘pay more, get more’. This differentiates, say, Lexus from Ferrari, or — to a lesser degree — Grand Seiko versus Patek Philippe. The risk with advertising new technology is to compromise the dream: if you get your customer evaluating your products in terms of objective functionality, you’d have dropped from a luxury designation back down to premium. The trick is to employ technology in service of the dream — which was exactly what Biver did here. Note again that this was all tacit at the time; in fact Donzé notes that various managers who worked under Biver in Omega later spread out across the watch industry and executed similar playbooks. In a very real way, SMH saved the Swiss watch industry because of the learning that occurred during its turnaround.

The second thing that Biver did was more straightforward. Just as with Blancpain, he tied Omega’s messaging to its long and illustrious history. This started from the very beginning of Biver’s tenure — as seen in how Omega emphasised its connection to the American space program at Basel in 1993 and 1994. In 1998, Omega published a 459 page book — the Omega Saga — to celebrate the 150th anniversary of the firm’s founding. The book focused on the development of sports chronometering (Omega was the official timekeeping partner of the Olympics for many of the Games, starting with Los Angeles in 1932) and celebrated Omega’s long history of awards obtained in chronometry contests, along with its — you guessed it! — participation in the Moon landing.

This emphasis on history has continued well past Biver: since 2010 Omega collectors may order extracts from Omega’s archives recounting the historical conditions in which their models were manufactured. Omega also started opening special sales outlets, starting with the Omega Vintage shop in London in 2008. The goal of all of these moves is to highlight the combination of historical tradition and technical excellence.

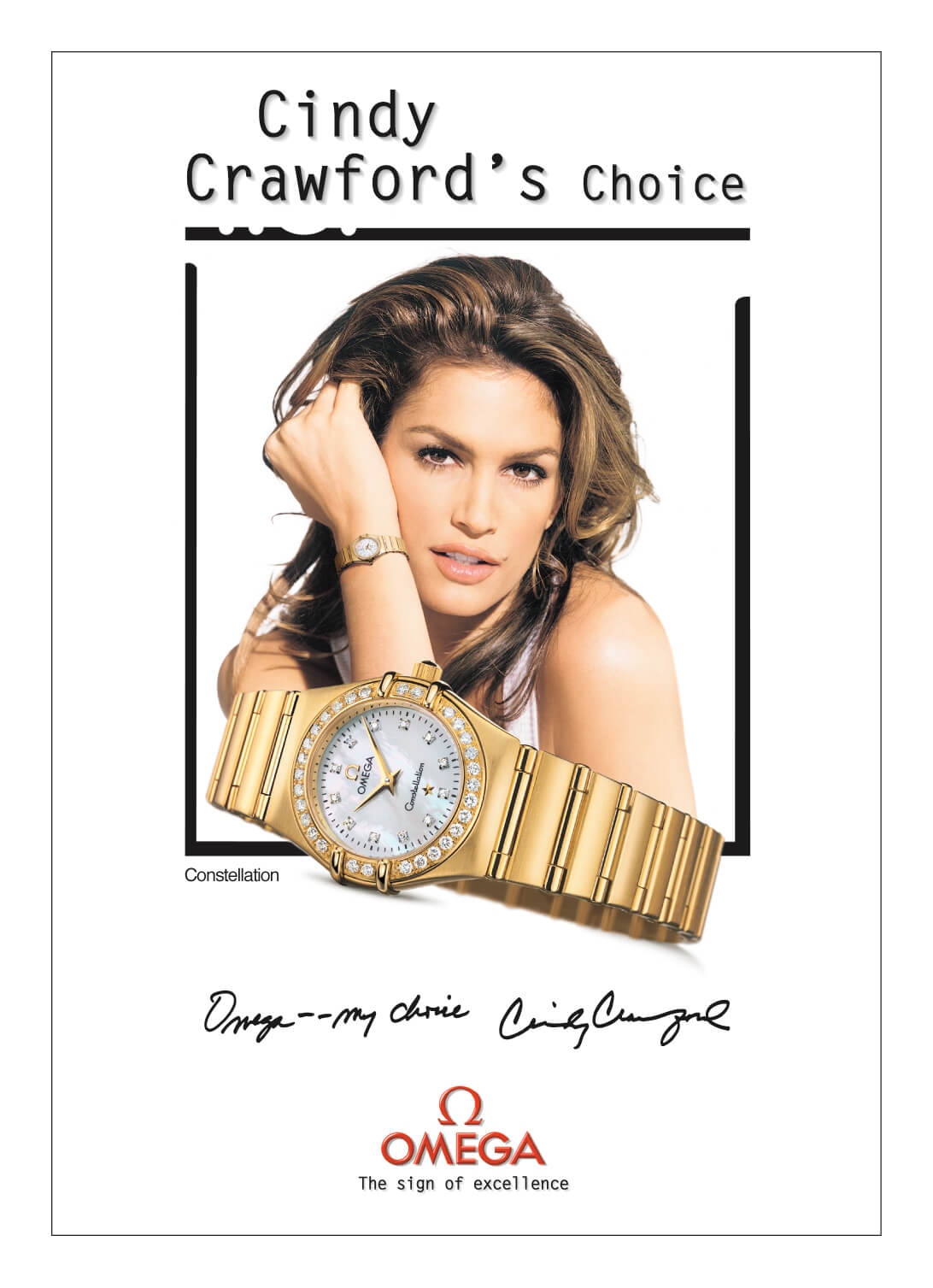

Finally, Biver started associating the Omega brand with glamour. Up to the middle of the 1990s, Omega’s advertising was product-centric, focusing on technical innovation and aesthetic appeal. It was also, as previously mentioned, image-based. Biver’s switch to message-based advertising allowed him to associate the product with celebrities. The most notable win for Biver was making Omega the watch brand of choice for James Bond in 1995, displacing Rolex. Biver also scored a win by drawing American supermodel Cindy Crawford into the brand; Crawford became actively involved in designing Omega watches for her own personal use — as Omega’s advertising took great pains to stress. The Constellation collection, for instance, became known as ‘Cindy’s Choice’ in Omega’s advertising of the period.

Here, again, Biver showed remarkable skill in brand construction. Later Kapferer and Bastien would explicate what he did, writing that it is important to “underline the difference between paying a star to appear in an advertisement and using a personality as a brand testimonial user. In the latter case … you show the extraordinary personality using the product in everyday life.” If the customer detects that the Hollywood star is but a model, paid to pose with the product, then this strategy would fail. Rather, the goal is again to enhance the dream: celebrities work best as ‘extraordinary testimonials for the use of a product’ — like Marilyn Monroe, who said that “a few drops of Chanel No. 5 were all she wore to bed.” (Or, one supposes, like James Bond, who casually wears an Omega Seamaster as he blows up the Bond villain).

Biver’s influence fundamentally changed the way Hayek ran his enterprise. The engineer-consultant who focused on supply chain efficiency, with almost no regard for the art of watchmaking, had seen what could be done when a great brand manager was in control. This change was most visible when Hayek decided to acquire and personally oversee high-end watchmaker Breguet.

For most of the 90s, SMH did not own high luxury brands. To bolster its luxury bonafides and increase the odds of Omega’s continued success, Hayek needed to buy brands at the tippy top of the market. Industry rumours of the time said that he had his eye on IWC, Jaeger-LeCoultre, and A. Lange & Söhne. Unfortunately, SMH simply could not afford these brands, for Hayek was hampered by his unwillingness to raise equity capital or to take out loans.

Hayek wanted total control of SMH. After the rationalisation of production freed up cash in the 80s, Hayek paid down SMH’s bank debt aggressively. SMH increased dividends to reward its shareholders (in particular the investors that Hayek had brought on to gain control of the company), but it also began piling up cash on its balance sheet at a remarkable rate.

Donzé describes this as follows (all bold emphasis added):

(…) the relentless growth in profits should not obscure a key element of the firm’s management: its self-financing policy. Modernization of the means of production and company growth went hand in hand with ever-diminishing reliance on banks. A huge amount of profit was ploughed back into reserves. Excluding paid-up capital, the Swatch Group’s accumulated equity capital came to a whopping CHF2.0 billion in 1995, compared with a scant CHF190 million in 1985 and 750 million in 1990. When measured as a percentage of the balance sheet, shareholders’ equity posted a rising trend until 1995. Whereas it was only 32.1 per cent in 1985, it passed the 50 per cent mark in 1989 and hit 70.1 per cent in 1995. This financial empowerment enabled the Swatch Group to develop without relying on bank loans. For Nicolas Hayek, who was only a minority shareholder in 1985, this strategy was the road to independence in the medium term. As for independence from the banks, their disinvestment from ASUAG and SSIH was an objective dating back to the 1970s. The development of the Swatch Group’s governance clearly reflects this process of emancipation, with the successive departure of most of the bankers from the Board of Directors: Rolf Beeler (BPS) and Paul Risch (BCB) in 1993, followed by Walter G. Frehner (SBS) in 1997. Since 1998, there has been only one banker on the Board: Peter Gross, a UBS director.

CHF2.0 billion was a lot of cash, but it was not enough to buy exclusive luxury watch brands at the top of the market. So Hayek changed his approach. Following Biver’s entry into SMH, Hayek realised that he could copy what Biver had done to Blancpain: buy up less famous brands with an impeccable historical pedigree, and then build them up. To this end Hayek bought four brands: Léon Hatot (1999), Breguet (1999), Jaquet Droz (2000), and Glashütte Uhrentriebe (2000), which the group quickly renamed Glashütte Original.

What followed surprised many who knew Hayek well. He took a hands-on approach to managing Breguet, immersing himself in the watchmaking process before deciding to commission the reconstruction of the Marie Antoinette watch, a legendary piece. Hayek was aware of the change others had seen in him, saying: “The purity of the watches, the complexity of their mechanisms, and [Breguet’s] splendid history captured my heart and my imagination.”

For his part, Biver had also been changed by his time with Hayek. A purist at heart, Biver had built up Blancpain by explicitly rejecting everything Hayek stood for with Swatch. No mass production. No compromise on quality. And of course, no quartz.

But whilst working under the SMH umbrella, Biver began to see the benefits of Hayek’s chosen strategy. Or perhaps he was persuaded by his peers in the Extended Group Management Board. During his second stint with Omega, Biver accepted mass production methods, and worked with both mechanical and quartz timepieces. Like Hayek, Biver possessed the self-awareness to notice the change, stating: “If you just retreat to luxury mechanicals, you’ll die. The Swiss watch industry was not saved by mechanical watches; it was saved by quartz watches.”

This was a remarkable admission by a man who had staked his entire career on exactly the opposite. Biver had come to understand that craft and tradition needed a production foundation to stand on. If nothing else, it sure generated a lot of cash.

The brand segmentation strategy worked once Biver turned Omega around. By the time Biver left Omega in 2003, he had nearly tripled its sales. In 2006, Omega made up 33.9% of the group’s revenue. As Hayek had believed for years, the cheap watch and the expensive watch relied on each other, forming a codependent, mutually beneficial relationship. The Swatch brand needed luxury brands above it to give it legitimacy. Omega — the affordable luxury brand — needed Swatch’s success to kickstart its turnaround. And the exclusive luxury brands at the top of the group’s portfolio provided a halo effect for all the brands below it. Together, they formed something Japanese competitors hadn’t — a complete market presence from $40 to $200,000 or more, all under the “Swiss-made” banner.

It wasn’t long before the SMH model became the template for the entire Swiss watch industry. In 1998, SMH renamed itself ‘The Swatch Group’. By the early 2000s, some of the country’s most prestigious brands had consolidated into competing groups along the same lines.

It is important to note that the Japanese brands, so dominant during the crisis years, started falling apart after Hayek and Biver got their marketing strategy to work. Donzé notes that the Japanese watchmakers never did seem to understand the luxury strategy — this so-called ‘non-technological innovation’ — that Biver executed. For years afterwards, Seiko continued pursuing technological innovation, culminating with the 1999 release of the quartz-mechanical hybrid Spring Drive movement — a remarkable technical achievement, accomplished after more than 20 years of research and development. Seiko continued to run image-heavy product-oriented advertising that extolled the wonders of its technical innovations. The company fell behind. This only began to change in the late 2010s, with Grand Seiko becoming its own independent luxury brand in 2017. Consequently, Casio, Seiko and Citizen all diversified beyond watches into electronics, as Japanese watch profits slumped in the face of the Swiss recovery.

The human legacy on the Swiss side was also far-reaching. Come 2008, several of Hayek and Biver’s protégés were CEOs of other Swiss watch brands, which together accounted for more than 50% of all Swiss watch sales. And it is the numbers that tell us that the strategy worked: by 2008, Swiss watchmakers accounted for 55% of global watch export value, matching the level they had in 1970, just before the crisis.

The Outcome

On the surface, it may have looked like a return to the status quo. It was anything but.

In 1970, Switzerland commanded 55% of the global market, while producing nearly half of the world’s total watches by volume. In 2008, it commanded the same revenue share while producing only 2% of global unit volume. The average export price of a Swiss watch was now $563, while that of an Asian-produced watch was just two dollars.

The scale of the recovery was staggering. The industry recorded 19 consecutive quarters of growth leading up to 2008. In 2009, Swiss watch exports totaled $11.5 billion, while Japanese watch exports amounted to just $0.6 billion. The Swatch Group alone commanded almost a quarter of the global watch market.

The turnaround was complete.

Sources

A primary source for this case was Pierre-Yves Donzé’s A Business History of the Swatch Group

https://www.theguardian.com/lifeandstyle/2010/jul/06/nicolas-hayek-obituary

https://theindex.nawcc.org/Articles/Watkins-JacquesDavid.pdf

https://hbr.org/1993/03/message-and-muscle-an-interview-with-swatch-titan-nicolas-hayek

https://www.hbs.edu/ris/Publication%20Files/16-003_be20d28e-23b9-4b58-a156-f3ae9c6c735f.pdf

https://www.theguardian.com/culture/2018/jan/08/how-we-made-the-swatch